New Congressional Effort to Rescue the American Dream Amid Escalating Housing Costs

The American dream of owning a home is now under serious scrutiny as a growing bipartisan group of House members rallies to tackle the escalating challenges of housing affordability in the United States. In what many are describing as a pivotal moment for the nation’s middle class, lawmakers have proposed a bill designed to put a spotlight on the many tangled issues that keep homeownership out of reach for too many Americans. This opinion editorial takes a closer look at the legislation’s goals, the complex mix of factors involved, and the broader implications for families, communities, and the economic fabric of our society.

While the official narrative is framed around “saving the American dream,” the proposed legislation aims to unearth the hidden factors hindering access to affordable housing. Far from a one-size-fits-all approach, the bill will establish an interagency task force that intends to gather more detailed information about mortgage costs, housing construction expenses, insurance premiums, down payment assistance, disaster resilience improvements, and federal housing finance programs. These are all essential measures designed to offer lawmakers and stakeholders a clearer picture of the confusing bits that blockade home purchases.

The discussion is not merely about numbers. It is a reflection on the personal struggles and systemic challenges many individuals and families face when trying to secure what has long been considered a quintessential part of building a stable, middle-class life. With rising home prices outpacing median household incomes, today’s working families find themselves grappling with off-putting financial obstacles, making the dream of owning a home seem increasingly out of reach.

Facing the Tricky Parts of Today’s Housing Market

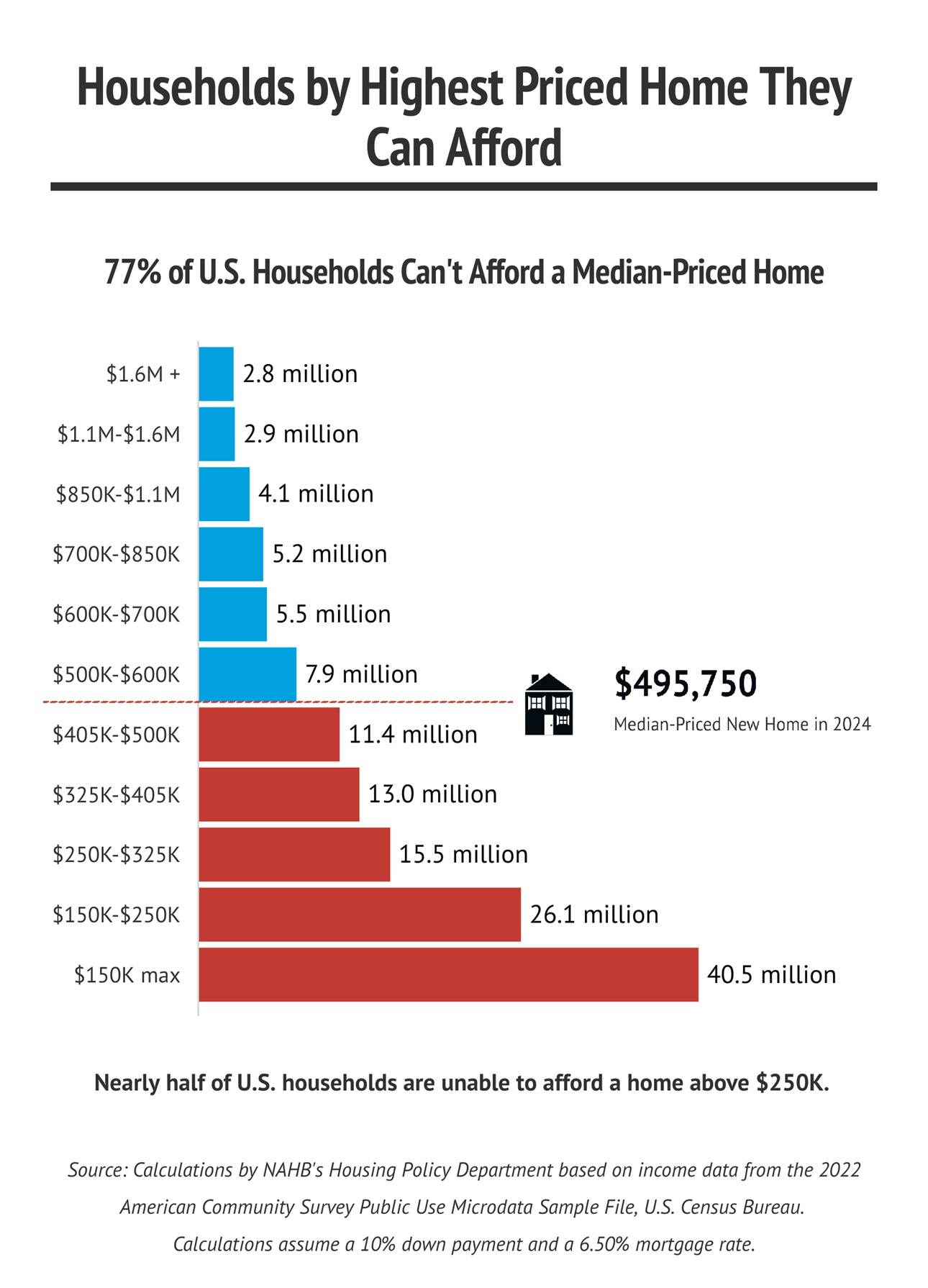

One of the most significant challenges lies in the tricky parts of our current housing market, where the rate of increasing housing prices far exceeds the growth in household incomes. Research from institutions such as the Urban Institute has shown that for a key demographic of 35-to-44-year-olds—many of whom are raising families and are in what should be their optimal homebuying years—the homeownership rate has dropped by more than 10% overall. This drop is not simply a numerical trend; it represents the tangible effects of policy shortcomings and market distortions that affect everyday Americans.

When we look at the broader picture, several intertwined factors come into play:

- Mortgage rates that remain high due to economic uncertainties.

- Rising construction costs connected to supply chain disruptions and increased material expenses.

- Escalating insurance premiums that add an extra layer of financial burden.

- Staggering down payment requirements often out of reach for many first-time buyers.

- Limited disaster resilience funding that leaves communities vulnerable in times of crisis.

Each of these components is part of a tangled web that makes it tough for families to secure adequate and affordable housing, thus perpetuating economic imbalances and social inequities.

Unpacking the Government’s Proposed Multiagency Task Force

The proposed bill calls for the creation of an interagency task force that will serve as a central repository for research and policy recommendations. Its main aim is to collect comprehensive data across multiple spectrums of the housing and mortgage industries. By doing so, the task force intends to unearth the fine points behind the costs and barriers that prospective homeowners are contending with.

This effort is set to involve several federal bodies, including:

- The U.S. Department of Housing and Urban Development (HUD), tasked with overseeing housing policies and ensuring quality standards.

- The U.S. Department of Agriculture, which plays a critical role in rural housing finance and community support.

- The Veterans Affairs department, which holds a unique perspective on housing for those who have served.

- The U.S. Department of the Treasury, a key player in shaping economic policies that directly impact mortgage rates and lending practices.

- The Federal Housing Finance Agency, responsible for supervising Fannie Mae, Freddie Mac, and other important elements of the housing finance system.

By pooling expertise from different agencies, the hope is to get into the nitty-gritty of each element of housing affordability. This multiagency approach promises to bring together diverse perspectives and crucial data so that policy makers can learn more about the small distinctions that cause broader market inequities.

How Mortgage, Construction, and Insurance Costs Are Intertwined

At the core of most affordability debates are the intertwined factors of mortgage, construction, and insurance costs. The proposed task force aims to sort out how each of these elements contributes to the overall challenge of buying a home. Many see these not as isolated bits of a larger problem, but rather as interconnected pieces that require a coordinated effort to address.

One critical area is mortgage affordability. With interest rates and lending standards fluctuating, the ability to secure a reasonable mortgage has become a nerve-racking endeavor for many would-be homeowners. The proposed initiative will look into how these rates tie into the overall cost of homeownership and whether adjustments in policy could ease these financial pressures.

Another equally important factor is construction. The cost of building a home has soared in recent years due to supply chain issues, increased labor costs, and regulatory changes that add delays and extra expenses. These construction costs naturally spill over into the final price that consumers must pay when purchasing a new home.

Insurance costs, too, have become overwhelming. With frequent natural disasters and climate uncertainty, insurance premiums have risen—not only affecting the cost of homeownership but also the long-term sustainability of owning property in certain regions.

In essence, solving one piece of the puzzle without considering the others may lead to incomplete or ineffective reforms. The federal task force is designed to break down these barriers in a way that encourages coordinated and balanced policy adaptations, ensuring that each of these tricky parts is given due attention.

Issues of Down Payment Assistance and Disaster Resilience: A Closer Look

A significant part of the affordability equation is linked to the challenge of down payments. For many first-time homebuyers, saving enough money for a down payment is a huge, intimidating hurdle. The bill under discussion does not only focus on traditional lending concerns but also looks to explore measures like down payment assistance programs. These programs, if properly designed and executed, could serve as a much-needed bridge for individuals aspiring to buy a home.

Moreover, the proposed legislation emphasizes the need for increased disaster resilience funding. In a time when natural disasters seem to be more frequent and severe, ensuring that homes are built or retrofitted to handle these events is both a safety imperative and an investment in long-term affordability. By incorporating disaster resilience into housing policy, lawmakers are acknowledging that the ability to withstand natural calamities can help prevent families from losing their homes when crisis strikes, ultimately supporting sustained homeownership in vulnerable areas.

Government-supported down payment assistance initiatives, combined with strategic investments in disaster-proofing communities, would not only make homeownership more accessible but also enhance the stability and safety of residential neighborhoods. This dual approach recognizes that simply addressing one issue while neglecting the other can lead to policies that are incomplete or even counterproductive.

Barriers Faced by the Middle Class in Achieving Homeownership

For too long, the middle class has been burdened by the increasing disparity between wages and the cost to purchase a home. Recent analyses indicate that even families with stable incomes and good credit are feeling the impact of a market where home prices have skyrocketed compared to median incomes. In California, for example, families now need to earn significantly more than they did just a few years ago to qualify for the median-priced home. This trend is symptomatic of deeper systemic issues within the housing market.

Some of the key barriers include:

- Employment challenges and stagnant wages that fail to keep pace with inflation and market demands.

- Rising costs associated with housing construction and maintenance.

- Increased credit standards and tighter lending requirements that favor established homeowners over newcomers.

- A shortage of available homes in areas with growing job opportunities, forcing many to compete in overheated markets.

These factors leave many middle-class families feeling like homeownership is no longer a realistic goal, but rather an increasingly elusive prize reserved for those who already possess significant financial resources. The proposed legislation serves as a reminder that the struggles of today’s middle class are not just economic statistics; they are lived realities impacting families across the country.

Personal Reflections on Homeownership and Social Mobility

For many individuals, the journey to homeownership is more than a financial transaction—it is a life-changing experience. Personal accounts often describe the period before owning a home as one filled with anxiety and the constant threat of eviction. As one representative recalling his own struggles noted, the transition from renting to owning can feel like a drastic change in lifestyle, marking the shift from merely surviving to truly thriving.

Stories from everyday Americans speak of families pooling every penny and enduring years of tough budgeting—sometimes sacrificing other essential needs—to save up for that all-important down payment. When those families finally make the leap into homeownership, it is seen as a moment of liberation and a marker of progress toward the middle-class dream. It’s about finding your way out of a cycle of perpetual renting, which many view as a temporary and unstable state, and moving toward a future where financial security and community roots are possible.

Yet, the stark reality is that for many young people today, the prospects of buying a home seem overwhelming and even unattainable in the current economic climate. The bill’s supporters argue that if new policies and more robust support systems can be implemented, there might be renewed hope that the dream can be revived—not just for an aging generation but for the young families of tomorrow as well.

The Role of Federal and State Policy in Revitalizing the Market

The interplay between federal and state policies plays a super important role in determining who gets to benefit from the potential solutions to housing affordability. For instance, states like California are living case studies in the challenges of an overheated market, where even small changes in economic policy can have dramatic effects on affordability. In these areas, the lack of robust down payment assistance programs and affordable financing options reinforces the cycle of exclusion for many would-be homebuyers.

State-level initiatives can work in tandem with federal reforms to create a more supportive environment for first-time buyers. Consider the following table, which outlines key areas of focus for both levels of government:

| Policy Area | Federal Strategy | State-Level Initiatives |

|---|---|---|

| Mortgage Lending | Review lending standards and adjust credit guidelines to encourage borrowing | Partner with local banks and community lenders to ease credit access |

| Construction Costs | Streamline regulatory processes and support supply chain improvements | Facilitate local permits and incentivize affordable housing developments |

| Down Payment Assistance | Fund national programs and research effective models | Implement state-specific grants and low-interest loan programs |

| Disaster Resilience | Invest in broader disaster preparedness and retrofit subsidies | Develop state-wide risk assessments and targeted resilience infrastructure |

This coordination is meant to foster a holistic approach, ensuring that every facet of the housing market is addressed and that overlapping responsibilities are aligned to create real, measurable impact. When federal and state authorities work together, they can create not only a more promising environment for potential homeowners but also a stronger safety net during times of economic or environmental upheaval.

Examining the Path Forward: Strategies for a Sustainable Housing Future

If the proposed bill is to have any lasting impact, it must pave the way for actionable solutions that address the practical challenges often hidden beneath the surface of housing statistics. Here are some strategies that could be key to unlocking a more sustainable and inclusive housing market:

- Enhancing Interagency Collaboration: By ensuring that agencies like HUD, the Treasury, and Agriculture work closely together, policymakers can better understand the full range of factors that affect affordability.

- Expanding Down Payment Assistance: Implementing robust programs at both the federal and state levels can help bridge the initial gap that prevents many households from entering the housing market.

- Improving Construction Efficiency: Addressing the off-putting twists and turns of the building process—such as unnecessary delays and regulatory roadblocks—can lead to reduced costs, thereby making homeownership more accessible.

- Boosting Insurance Support: Innovative approaches to managing risk and subsidizing insurance for first-time buyers could mitigate one of the nerve-racking aspects of homeownership.

- Investing in Disaster Resilience: Ensuring that new developments and existing communities are better prepared for natural disasters will protect families from having to rebuild repeatedly, preserving the long-term value of their investments.

In addition to these strategies, lawmakers and advocates need to maintain an ongoing dialogue with both the private sector and community organizations. This will help ensure that the solutions being crafted are not only theoretically sound but also practically applicable in communities across the nation. The goal is not merely to collect data but to transform that information into policies that work on the ground, making it easier for families across socio-economic levels to build secure, lasting homes.

Why Recognizing the Little Details is Essential for Effective Legislation

The success of any legislative effort often lies in the small details—the subtle parts that, while seemingly minor, can have a transformative effect on the way policies play out in real life. In the realm of housing, these little details include the specific eligibility requirements for assistance programs, the criteria for assessing mortgage risk, and the protocols for disaster preparedness funding.

For example, it is not enough to simply allocate funds for down payment assistance; such programs must be designed with a keen understanding of local market conditions and the diverse needs of applicants. That means digging into the nitty-gritty of local housing markets, tailoring assistance programs that are flexible enough to meet the needs of urban centers and rural communities alike, and ensuring that support measures are continuously updated to respond to evolving challenges.

Similarly, when considering construction costs, it is crucial to recognize that regulatory improvements and supply chain efficiencies can vary significantly from one region to another. Policymakers need to figure a path that acknowledges these small distinctions and leverages local expertise to implement more streamlined, cost-effective processes for approving and building new homes.

This keen attention to the little details is not just a bureaucratic necessity—it is a practical way to ensure that policy reforms do more than just sound good on paper. They must work in the everyday lives of those who are striving to secure a safe and stable home for themselves and future generations.

The Impact on Younger Generations and Long-Term Socioeconomic Mobility

When discussing housing affordability, it is impossible to overlook the perspective of younger generations who are steadily being priced out of markets that were once considered gateways to prosperity. For many young people, the dream of owning a home has shifted from a clear and attainable goal to an increasingly hazy notion, overwhelmed by economic uncertainty and the heavy burden of student debt.

This trend has profound implications for long-term socioeconomic mobility. Homeownership has traditionally been a key driver of wealth accumulation and a symbol of economic stability in the United States. The equity built into a home often serves as a springboard for further investments, education, and even retirement planning. When younger generations are unable to own homes, this can lead to a cycle of financial instability and reduced upward mobility, perpetuating gaps between economic classes.

Many critics point out that while the current market dynamics might encourage spending on travel and experiences in the short-term, they also risk undermining the traditional paths to building lasting wealth. For instance, the benefits of having a substantial line of credit or building equity over time might seem less attractive when the initial hurdle of acquiring a home is so daunting and expensive.

Addressing this issue requires a willingness to consider policies that not only ease the immediate financial strain but also look further ahead. How do we nurture an environment in which young families can see homeownership as a reachable goal? The answer lies in a multifaceted approach that combines financial support, regulatory reforms, and educational initiatives aimed at demystifying the process of buying a home, making it less intimidating and more within reach for future generations.

Community Perspectives: Weighing the Pros and Cons of Government Intervention

The proposed congressional initiative has sparked a wide range of reactions among community leaders, potential homebuyers, and economic experts alike. On one hand, supporters of the bill argue that such comprehensive measures are long overdue given the staggering rise in housing costs and the corresponding squeeze on middle-class families. They contend that without bold action, the dream of homeownership will continue to slip away from countless Americans.

Critics, however, raise concerns about the scope of government intervention. Some worry that increasing the reach of federal agencies in local housing markets might lead to overregulation or create unintended ripple effects that could stifle innovation in the private sector. Others caution that even well-intentioned programs might struggle to address the fundamental supply and demand issues that have contributed to the current housing crisis.

The debate is further complicated by differing regional realities. Urban centers facing hyper-competitive housing environments may benefit from aggressive federal programs, while rural areas with limited housing stock might require different strategies tailored to their unique challenges. The bipartisan nature of the proposed task force, with representatives from varied backgrounds and constituencies, suggests that there is broad recognition of these concerns—even if opinions differ on the best way to move forward.

In order to balance these views, it is important that any government-led intervention remains flexible and responsive. Regular consultations with local community organizations, real estate professionals, and financial experts will be critical in ensuring that the policies enacted under this bill are both practical and effective. Only by maintaining an open dialogue can lawmakers hope to steer through the nerve-racking twists and turns of modern housing markets and deliver a solution that works for all.

Lessons from the Past: Historical Insights into Housing Policy Reforms

Looking back at previous housing policy reforms, it becomes evident that well-meaning legislative efforts have sometimes fallen short due to their inability to address all the little details. Historical examples, such as the post-World War II housing boom and the subsequent suburban expansion, illustrate how government policies can simultaneously drive economic growth and foster unintended disparities within communities.

In those earlier eras, federal initiatives helped millions of families secure homes, yet they also laid the groundwork for problems such as urban sprawl and socioeconomic segregation. These outcomes remind us that even the most comprehensive reforms can be loaded with issues if they do not consider the full spectrum of economic, environmental, and social impacts.

Today’s challenge is to find a balance—creating policies that simultaneously encourage economic vitality, protect consumers, and ensure that the benefits of homeownership are accessible to all. The current proposal seeks to avoid past pitfalls by emphasizing coordination between multiple government agencies, hoping that a more integrated approach can better manage the confusing bits associated with housing affordability. By learning from previous experiences, lawmakers can strive to design reforms that are both pragmatic and forward-looking.

Strategies for a Resilient Housing Market: What Needs to Change?

Building a resilient housing market in today’s economic environment requires an honest assessment of what has and has not worked in the past, as well as a willingness to experiment with new ideas. Here are some potential avenues for change:

- Data-Driven Decision Making: By establishing an interagency task force, the proposed legislation seeks to dig into extensive datasets that capture the small distinctions and subtle parts of the housing market. With accurate and timely data, policymakers can make informed decisions that address specific pain points rather than applying blanket solutions.

- Tailored Financial Incentives: Instead of a one-size-fits-all approach, financial incentives need to be tailored to meet the unique needs of different regions and demographic groups. For example, urban areas facing extremely high property prices might need different forms of credit support compared to rural communities where supply issues are more pressing.

- Modernizing Regulatory Processes: Streamlining zoning laws, permitting procedures, and construction regulations can help reduce unnecessary delays and lower construction costs. Simplifying these processes can help reduce the overall cost of homeownership and make the process less intimidating for developers and buyers alike.

- Community-Based Solutions: Involving local communities in policy design ensures that their unique challenges and needs are considered. Initiatives like cooperative housing models or public-private partnerships can foster local investment and encourage innovative, community-driven solutions.

- Investing in Workforce Development: Expanding job training and education programs in the construction, real estate, and finance sectors can help create a more robust and adaptable housing market. A skilled workforce is essential for reducing the off-putting complexities of modern housing construction and maintenance.

Each of these strategies highlights the need for a nuanced, flexible approach to reforming housing policy. Rather than being overly prescriptive, the suggested measures are designed to adapt to changing conditions and regional differences, ensuring that policy reforms remain effective over time.

Looking Ahead: The Future of Homeownership in America

The current legislative push to address housing affordability represents not just a response to a crisis but a potential turning point in the nation’s approach to homeownership. If successful, it could redefine how policies are formulated and implemented in the years to come. By making concerted efforts to address the complicated pieces related to mortgage financing, construction costs, insurance fees, down payment hurdles, and even disaster preparedness, this initiative could serve as a model for future reforms.

The long-term benefits of such a comprehensive approach are numerous. For one, a more accessible housing market can help stabilize communities by reducing the risk of homelessness and bolstering middle-class stability. Moreover, increased homeownership has the potential to generate broader economic benefits, from enhanced consumer spending to improved overall public health and well-being.

However, achieving these benefits will require sustained effort and a willingness to work through the nerve-racking twists and turns inherent in any complex policy area. Lawmakers, community leaders, financial experts, and individual families alike must remain committed to finding innovative solutions and adapting them as challenges evolve. Only with perseverance and a collaborative spirit can the promise of the American dream be reimagined for the 21st century.

Conclusion: A Call for Collaborative, Detail-Oriented Reform

In conclusion, the bipartisan congressional effort to form a dedicated task force on housing affordability marks an important step toward addressing one of America’s most pressing economic challenges. By focusing on the small distinctions and hidden complexities that impede homeownership, the legislation offers a promising framework for mitigating some of the overwhelming obstacles faced by many families today.

This isn’t just a policy debate; it’s a discussion about the future of our communities, the well-being of our middle class, and the enduring promise of the American dream. While the road ahead may be loaded with issues and the process of implementing change may be intimidating at times, a collaborative and detail-oriented approach is essential. The task force, by uniting experts from multiple federal agencies and working closely with local stakeholders, seeks to figure a path that not only clarifies the underlying challenges but also charts a course for a more secure and affordable future.

Ultimately, success will depend on our collective willingness to adapt, innovate, and invest in solutions that address both the visible and hidden obstacles to homeownership. As we continue to witness rising costs and shifting economic realities, it is super important to remember that effective reform is often found in the willingness to tackle the little details—those tiny twists that, when resolved, pave the way for lasting change. Let this initiative be a rallying cry for concerted, practical, and empathetic policymaking that honors the spirit of community and the enduring pursuit of the American dream.

Originally Post From https://www.columbian.com/news/2025/sep/22/theres-a-new-congressional-effort-to-address-housing-affordability/

Read more about this topic at

Saving the American Dream Act: A New Path Forward for ...

Mann, Alford, Real Estate Caucus Co-Chairs Introduce Saving ...

Social Plugin